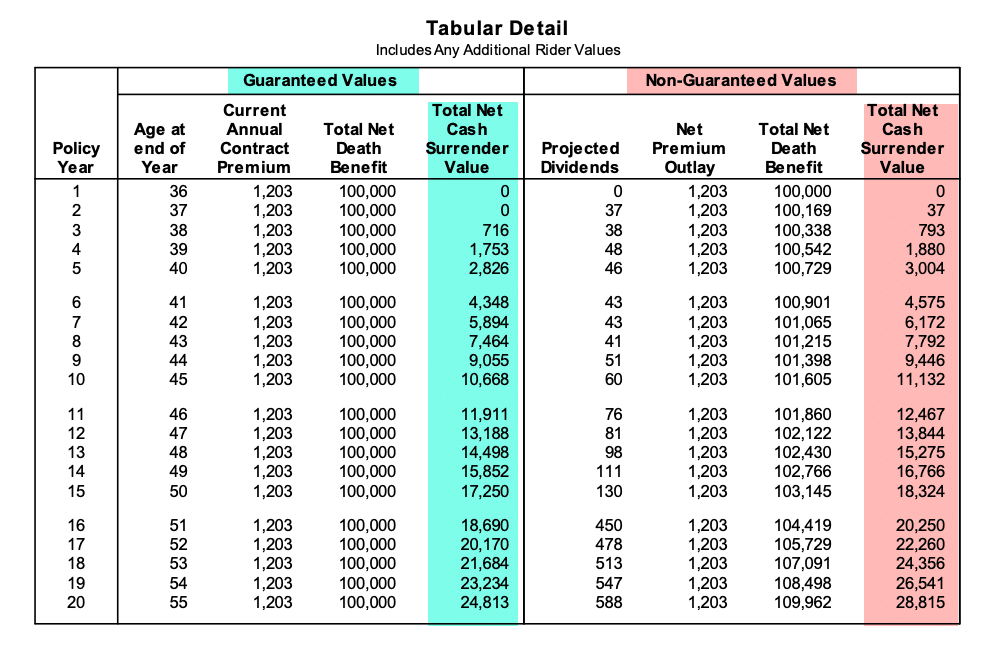

Understanding Whole Life Insurance: Benefits You Should Know

Whole life insurance is a type of permanent life insurance that provides coverage for the insured's entire life, as long as the premiums are paid. One of the primary benefits of whole life insurance is its cash value component, which accumulates over time. This cash value can serve as a savings vehicle, allowing policyholders to borrow against it or withdraw funds if needed. Additionally, whole life insurance features predictable premiums that do not increase as the insured ages, providing stability and peace of mind. For more information on whole life insurance, visit Investopedia.

Moreover, many whole life insurance policies offer dividends paid out to policyholders, which can be reinvested to increase the cash value or used to offset premiums. This aspect of whole life insurance can create a sense of financial security, as policyholders not only secure life coverage but also build wealth over time. It's important to understand how these benefits align with your financial goals and needs. To explore the potential advantages further, check out the detailed analysis on NerdWallet.

Is Whole Life Insurance the Right Choice for Your Financial Future?

When considering your financial future, whole life insurance can be an appealing option for many individuals. It offers a unique blend of life coverage and a savings component, allowing you to build cash value over time. Unlike term life insurance, which only provides coverage for a specific period, whole life insurance remains in force for your entire lifetime, provided premiums are paid. This makes it a stable financial instrument that can serve multiple purposes, including estate planning and creating a legacy for your beneficiaries. For more detailed information, check out Investopedia.

However, it's essential to weigh the pros and cons before making a decision. While whole life insurance can offer guaranteed benefits, it typically comes with higher premium rates compared to term life policies. Additionally, the growth of cash value is often slower than other investment alternatives. To determine if whole life insurance is right for you, consider your financial goals, risk tolerance, and how you intend to utilize the cash value. Consult financial advisors or resources such as NerdWallet to help guide your decision-making process.

Unlocking the Myths: What Whole Life Insurance Really Offers

Whole life insurance has always been surrounded by a cloud of myths and misconceptions that can lead potential policyholders astray. Many people assume it is just a costly and irrelevant financial product, while others misunderstand its purpose. In reality, whole life insurance provides not only lifelong coverage but also a cash value component that can serve as a financial asset over time. As premiums are consistently paid, a portion is allocated to the cash value, which grows at a guaranteed rate. This unique feature allows policyholders to borrow against their policy or withdraw funds, making it a versatile addition to one’s overall financial strategy.

Another common myth is that whole life insurance is too expensive compared to term life insurance. While it does come with a higher premium, it’s essential to recognize the long-term benefits it offers, such as stability and predictability in both coverage and cash value growth. In fact, the cash value accumulates on a tax-deferred basis, allowing policyholders to potentially access funds for investment or emergencies without immediate tax implications. Understanding these benefits can help individuals navigate the complexities of their financial futures and recognize that whole life insurance could play a pivotal role in a well-rounded financial plan.